What’s Changing and How to Plan Ahead

As we step into 2025, tax updates are at the forefront of financial planning conversations, particularly for those nearing retirement. This year brings a mix of inflation adjustments, policy shifts, and potential legislative changes that could impact how much you owe and how you should plan your finances.

Nelson Financial Planning recently discussed these updates in their Dollars & Sense podcast, emphasizing the key takeaways every taxpayer should be aware of.

Let’s dive into the most important tax changes and strategies to keep more of your hard-earned money.

Top 10 Tax Changes for 2025

- Tax brackets are adjusted for inflation

- Standard deduction increases again

- Expiration of the 2017 tax cuts and jobs act (TCJA)

- Higher retirement contributions

- Required minimum distributions (RMDs) stay at 73, but new rules apply

- 1099-K reporting threshold lowered

- Estate and gift tax exemption rises

- Roth employer match now available

- IRS underpayment penalty reduced

- State law changes – some lowering income tax rates and others expanding tax credits for retirees

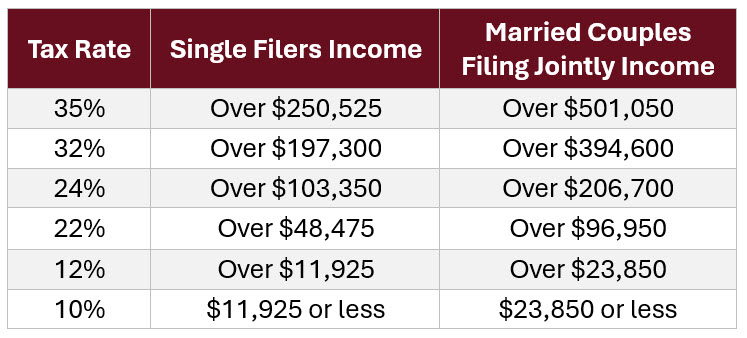

Tax Change #1: Tax Brackets are Shifting Upwards

Each year, tax brackets adjust to prevent “bracket creep” – where inflation pushes taxpayers into higher brackets. In 2025, income thresholds will increase slightly, which may lower tax liabilities for some individuals.

WHAT THIS MEANS FOR YOU

- You may pay slightly less in taxes if your income remains steady

- If you’re close to a higher bracket, tax planning could help lower your taxable income

WHAT YOU SHOULD DO

- Adjust your withholding or estimated tax payments if needed

- Consider maximizing tax-deferred accounts like 401(k) to lower taxable income

- Consult a tax professional to ensure you take full advantage of bracket shifts

Tax Change #2: Standard Deduction Increases Again

The standard deduction has increased to $15,000 for single filers and $30,000 for married couples filing jointly. Those 65 and older receive an additional deduction.

IMPACT ON YOU

- More income can be deducted without itemizing, simplifying the filing process

- If the TCJA expires in 2025, the standard deduction may be cut in half, leading to higher taxable income for many taxpayers

WHAT YOU SHOULD DO

- Compare standard vs itemized deductions to ensure you claim the highest deduction possible

- If you are planning large deductible expenses, consider timing them to maximize your tax benefits

- Stay informed about potential legislative changes that could impact deductions

Tax Change #3: Expiration of the 2017 Tax Cuts & Jobs Act (TCJA)

One of the most significant potential changes is the Tax Cuts and Jobs Act (TCJA) expiration at the end of 2025. If Congress does not extend these provisions, tax rates will revert to pre-2017 levels meaning:

- The 12% tax bracket increases to 15%

- The 22% bracket jumps to 25%

- The top tax rate returns to 39.6% from 37%

- The $10,000 cap on SALT deductions could be eliminated, impacting high-tax states

Pre-2017 Tax Rates

“Looking at individual rates now, we are in brackets that are 10, 12, 22, 24, 32, 35, and 37%. Moving forward, each bracket except the 10% bracket is going to go up about 2 or 3%,” said Kristin Castello, Certified Financial Fiduciary at Nelson Financial Planning.

IMPACT ON YOU

- Higher tax rates would mean increased tax liabilities for most filers

- Business owners may lose benefits like the qualified business income (QBI) deduction, leading to higher taxable income

WHAT YOU SHOULD DO

- If possible, accelerate income into 2025 while tax rates are lower

- Consider a Roth IRA conversion in 2025 to lock in lower tax rates

- Work with a financial advisor to adjust your tax strategy

Tax Change #4: Higher Retirement Contribution Limits

Retirement savings account limits are increasing to keep pace with inflation:

- 401(k) contribution limits rise to $23,500

- IRA contribution limits remain at $7,000

- Catch-up contributions increase to $11,250 for ages 60-63

IMPACT ON YOU

- Increased limits provide more opportunities for tax-advantaged savings

- Those nearing retirement age (60-63) get an extra boost in catch-up contributions

WHAT YOU SHOULD DO

- Max out contributions if possible to take full advantage of tax benefits

- If you are age 60-63, consider increasing catch-up contributions to boost savings

- Work with your employer to ensure they are implementing these new limits

Tax Change #5: Required Minimum Distributions (RMDs) Stay at 73 but New Rules Apply

The RMD penalty decreases from 50% to 25%, or 10% if corrected quickly. And inherited IRAs much now be fully withdrawn within 10 years.

IMPACT ON YOU

- Lower penalties make it easier to correct missed RMDs without severe consequences

- Beneficiaries of inherited IRAs may need to withdraw funds faster, increasing taxable income

WHAT SHOULD YOU DO

- Set up automatic RMD withdrawals to avoid penalties

- If you inherited an IRA, consult a financial planner to ensure you meet distribution requirements

- Consider charitable giving strategies (like Qualified Charitable Distributions) to satisfy RMDs tax-efficiently

Tax Change #6: 1099-K Reporting Threshold Lowered

The IRS has significantly lowered the reporting threshold for 1099-K forms from $20,000 and 200 transactions to $600 in total transactions. This means more people will receive tax documents for online sales.

“Many small business owners and even individuals selling used items online will need to be more aware of their tax obligations,” said Kristin Castello.

IMPACT ON YOU

- Even casual sellers on Venmo, Paypal, or eBay could receive a tax form

- You may owe taxes if your sales exceed your cost basis (what you originally paid for the items)

WHAT YOU SHOULD DO

- Keep detailed records of purchase prices and sales amounts to prove taxable gains or losses

- If you receive a 1099-K even if in error be sure to appropriately report it on your tax return

- Consult a tax professional to ensure you properly report income and avoid IRS scrutiny

Tax Change #7: Estate & Gift Tax Exemptions Rise

The estate tax exemption has increased to $13.99 million per individual, and the annual gift tax exclusion has risen to $19,000 per recipient.

IMPACT ON YOU

- Wealthier individuals can transfer more money tax-free to heirs and beneficiaries

- Fewer estates will be subject to federal estate taxes

WHAT YOU SHOULD DO

- Consider making larger tax-free gifts now to reduce your taxable estate

- Work with an estate planner to optimize wealth transfer strategies

- Utilize trusts and other financial tools to protect family wealth

Tax Change #8: Roth Employer Match Now Available

Employers can now offer Roth 401(k) matching contributions, meaning employees can receive tax-free growth on matched funds.

“This change gives workers more flexibility in choosing their tax strategies for retirement,” Castello added.

IMPACT ON YOU

- Roth matches are taxed now but grow tax-free, unlike pre-tax employer matches

- Your retirement withdrawals could be entirely tax-free

WHAT YOU SHOULD DO

- Check with your employer to see if they offer Roth matching options

- If you’re in a lower tax bracket now, opting for Roth contributions could benefit you in retirement

- Adjust your retirement savings strategy to maximize tax-free income

Tax Change #9: IRS Underpayment Penalty Reduced

The IRS underpayment penalty is decreasing from 8% to 7%, offering a small relief for those who owe estimated taxes.

IMPACT ON YOU

- If you underpay your taxes, you’ll owe slightly less in penalties

- Quarterly estimated taxpayers, including retirees and self-employed individuals, will benefit the most

WHAT SHOULD YOU DO

- Adjust estimated tax payments to avoid penalties

- Use the IRS tax withholding estimator to ensure proper withholding

- If you frequently owe at tax time, increase paycheck withholding to avoid penalties

Tax Change #10: State Tax Law Changes

Several states are adjusting tax policies, with some lowering income tax rates and others expanding tax credits for retirees.

IMPACT ON YOU

- Your state tax burden may change depending on where you live

- Some states are shifting towards flat tax systems, impacting retirees and high-income earners

WHAT YOU SHOULD DO

- Review your state’s tax law changes and how they impact your retirement plan

- If considering relocation, compare state tax policies on pensions and social security

- Work with a financial planner to optimize your tax strategy based on state-specific changes

Frequently Asked Questions

Q: What are the federal income tax brackets for 2025?

A: For 2025, the seven federal income tax brackets are 10%, 12%, 22%, 24%, 32%, 35%, and 37%. For married filing jointly, the 12% bracket applies to income from $23,200 to $94,300, and the 22% bracket applies from $94,300 to $201,050. Single filers enter the 22% bracket at $47,150. These amounts reflect the IRS’s inflation adjustment for 2025. Most retirees with combined income under $94,300 (MFJ) remain in the 12% bracket — which has significant implications for Roth conversion strategy before RMDs begin at age 73.

Q: How do the 2025 tax changes affect retirees?

A: For 2025, inflation adjustments to tax brackets, the standard deduction, and retirement account contribution limits all benefit retirees. The standard deduction increased to $30,000 for married couples filing jointly. The SECURE 2.0 Act also continued its phase-in: the RMD starting age remains 73 for anyone born between 1951 and 1959, and rises to 75 for those born in 1960 or later. Additionally, the enhanced catch-up contribution limit for ages 60-63 increased to $11,250 for 401(k) plans — a meaningful opportunity for pre-retirees in their early 60s.

Q: Did the standard deduction increase for 2025?

A: Yes. The standard deduction for 2025 is $30,000 for married couples filing jointly (up from $29,200 in 2024) and $15,000 for single filers (up from $14,600). For taxpayers 65 and older, an additional standard deduction applies: $1,550 per person (married filing jointly) or $1,950 (single). For most retirees, the combination of the standard deduction and age-related additions makes itemizing unnecessary — which simplifies tax preparation but also affects the value of certain deductions like mortgage interest.

Q: What is the capital gains tax rate for 2025?

A: For 2025, the 0% long-term capital gains tax rate applies to married couples with taxable income up to $96,700 and single filers up to $48,350. The 15% rate applies above those thresholds up to $583,750 (MFJ) or $533,400 (single). For retirees managing portfolio withdrawals and Roth conversion strategy, staying within the 0% capital gains bracket is a meaningful tax planning opportunity — particularly in years between retirement and the onset of Required Minimum Distributions.

Q: How do 2025 tax brackets affect Roth conversion decisions?

A: The 2025 tax brackets create a planning window for retirees in the gap years between retirement and age 73 when RMDs begin. If your taxable income in 2025 keeps you in the 12% bracket (up to $94,300 for married filers), a partial Roth conversion at 12% may be significantly better than paying 22% or higher later when RMDs force larger withdrawals. The 2025 standard deduction of $30,000 also means many retirees can convert more than they might expect while staying in a favorable bracket. Nelson Financial Planning’s team models this conversion window for every client — including the IRMAA impact of any income increase.

Q: Will the 2025 tax rates expire?

A: The current individual income tax rates were established by the Tax Cuts and Jobs Act of 2017. Several provisions were extended through 2025 tax year changes and the One Big Beautiful Bill passed in 2025-2026 made certain rates permanent or modified them. The senior deduction of $6,000 per person (for those 65 and older) applies for tax years 2025 through 2028. Changes to Social Security taxation and tip income deductions were also introduced. Nelson Financial Planning’s Dollars & Sense podcast covers each major change as it is enacted — subscribe at www.NelsonFinancialPlanning.com.

Final Thoughts

2025 will be a year of significant tax changes, with potential increases looming. Being proactive now can help you minimize tax burdens and maximize savings.

For expert financial guidance, contact Nelson Financial Planning today!

TAKE CONTROL OF YOUR FINANCES.

Unlock the secrets to financial success with Joel J. Garris’ insightful book, designed to equip you with the essential tools and strategies needed to take control of your financial future.

REQUEST YOUR FREE COPY OF OUR BOOK – NEXT GEN DOLLARS & SENSE

ABOUT THE AUTHOR

Christina Lamb · IRS Enrolled Agent & Certified Financial Fiduciary™

Christina is an IRS Enrolled Agent — a designation granted by the IRS itself that authorizes her to represent clients directly before the IRS. She is one of the very few advisors in Central Florida who brings this level of tax expertise directly into a financial planning practice. At Nelson Financial Planning, she coordinates tax strategy alongside investment planning for every client.

Reviewed by Joel Garris · CFP® & Certified Financial Fiduciary™

- 8 Wonders1

- Bank Investments3

- Beating Inflation1

- Budget for Retirement5

- Corporate Transparency Act2

- Digital Currency1

- Energy Tax Credits1

- ESG Funds1

- Featured Blog0

- Financial Planning14

- Financial Success5

- Importance of Dividends1

- Investment Diversification1

- Investment Portfolio6

- Investment Strategy4

- IRA1

- Joel Garris1

- Nelson Financial Planning7

- Net Worth Improvement1

- Next Gen Dollars and Sense1

- One Big Beautiful Bill Act (OBBBA)1

- Pension Plans1

- Podcast Transcripts17

- Retirement “Secure” Act2

- Retirement Income Planning3

- Retirement Planning7

- Retirement Regrets5

- Social Security4

- Tax Liability3

- Tax Planning7

- Year-End Tax Changes3