Florida Retirement System

Your Complete Planning Guide for State Employees

Written by: Joel Garris, CFP® & Certified Financial Fiduciary™ | 25+ Years of Retirement Planning | Nelson Financial Planning

Joel and the Nelson Financial Planning team have guided Florida government employees — teachers, law enforcement officers, firefighters, and state workers — through FRS decisions for decades. There are no account minimums, which means every FRS employee has access to the same quality of guidance regardless of salary or years of service.

40+ Years Serving Central Florida · Certified Financial Fiduciaries™ · We Wrote the Book on FRS — Now in Its 5th Edition · No Account Minimums

The FRS election is permanent for most members. Making it without a full analysis - one that includes survivor benefits, DROP timing, and how FRS fits into your overall income plan - is one of the most common planning mistakes Nelson Financial Planning sees.

If you are a Florida teacher, law enforcement officer, firefighter, or state or county government employee, you are eventually going to face one of the most consequential financial decisions of your career: the FRS election.

The Florida Retirement System gives eligible employees the ability to choose between two fundamentally different retirement structures — the FRS Pension Plan and the FRS Investment Plan. You get exactly one second election to switch between them during your entire career, and several related decisions — entering DROP, selecting a survivor option, rolling over a payout — are permanently irreversible. And most financial advisors you might turn to for help don't understand FRS well enough to guide you through any of it.

Nelson Financial Planning has been serving Florida government employees since 1984 — and literally wrote the book on the system. The State of Your Retirement: The Essential Guide for All State of Florida Employees, now in its 5th edition, covers the Pension Plan, the Investment Plan, DROP, and every major legislative change since 2008. These conversations have always been a free service to state employees — no consulting fees, no account minimums — and the weekly Dollars & Sense podcast keeps members current on every FRS development between editions.

The guides in this section are built from the team's actual work with FRS members. This is the most complete FRS planning resource available from an independent, fiduciary financial advisor in Central Florida.

The FRS Pension Plan: The Guaranteed Check-a-Month

The FRS Pension Plan is a defined benefit plan backed by the State of Florida. Your monthly retirement income is determined by a formula: years of creditable service multiplied by a service credit percentage, then multiplied by your Average Final Compensation. That check is guaranteed to last your lifetime — regardless of market conditions.

There are four payout options. Option 1 generates the highest monthly income but ends when you die. Option 3 continues a lifetime benefit to your spouse after your death, at a monthly amount typically 15 to 20 percent lower depending on your spouse's age. Option 2 guarantees payments for at least 10 years, and Option 4 allows dependent or disabled children to be included as contingent recipients. The option you select at retirement cannot be revisited — and over a 30-year retirement, the trade-offs are significant.

One detail many members don't learn until retirement: the cost-of-living adjustment. The 3% annual COLA was suspended for all service after July 1, 2011, and has never been reinstated for most members. Your COLA in retirement is a blend — years of pre-2011 service at 3%, years after at 0%, averaged across your career. A member retiring recently with 25 years of service might see a permanent COLA of roughly 1.2% rather than 3% — a meaningful difference in purchasing power over decades of rising prices. And a 2026 change is genuinely good news for retired deputies, firefighters, and other Special Risk Class members: effective July 1, 2026, eligible special risk retirees who have been retired at least five years receive a minimum 1.5% annual cost-of-living adjustment — the first COLA improvement since the 2011 suspension. Members enrolled before July 2011 get the greater of 1.5% or their blended formula rate; those enrolled after get the flat 1.5%. Eligibility requires six years of Special Risk Class service (eight for those enrolled after July 1, 2011), and the adjustment applies with each July benefit payment.

The rules also differ by hire date. Employees hired after July 1, 2011 face a higher normal retirement age (65 or 33 years of service for regular class), an eight-year vesting period instead of six, and the 3% employee contribution that applies to all members. One bright spot: the 2023 legislature restored the special risk class normal retirement age to 55 or 25 years of service.

What the Pension Plan does not offer is lump-sum access. Your FRS pension provides monthly income — not a pool of capital you can draw from for large expenses, leave to beneficiaries, or invest differently. For some members, that limitation matters. That's where DROP becomes relevant.

The FRS Investment Plan: Flexibility with a Different Kind of Risk

The FRS Investment Plan is a defined contribution plan.

Your employer contributes a set percentage of your salary based on your membership class, and your own required 3% contribution goes into your personal account rather than the general FRS fund. The account vests in just one year — dramatically faster than the Pension Plan. You direct your own investments from a menu of roughly 20 options.

The flexibility is real. Investment Plan balances are portable, can be left to a spouse or children — your years of FRS service represented entirely in a cash value lump sum — and give you control over investment decisions. The risk is also real: there is no guaranteed income floor. Your retirement income depends entirely on investment performance, and the balance must be managed to generate monthly income for life. It cannot be treated like a cookie jar in retirement.

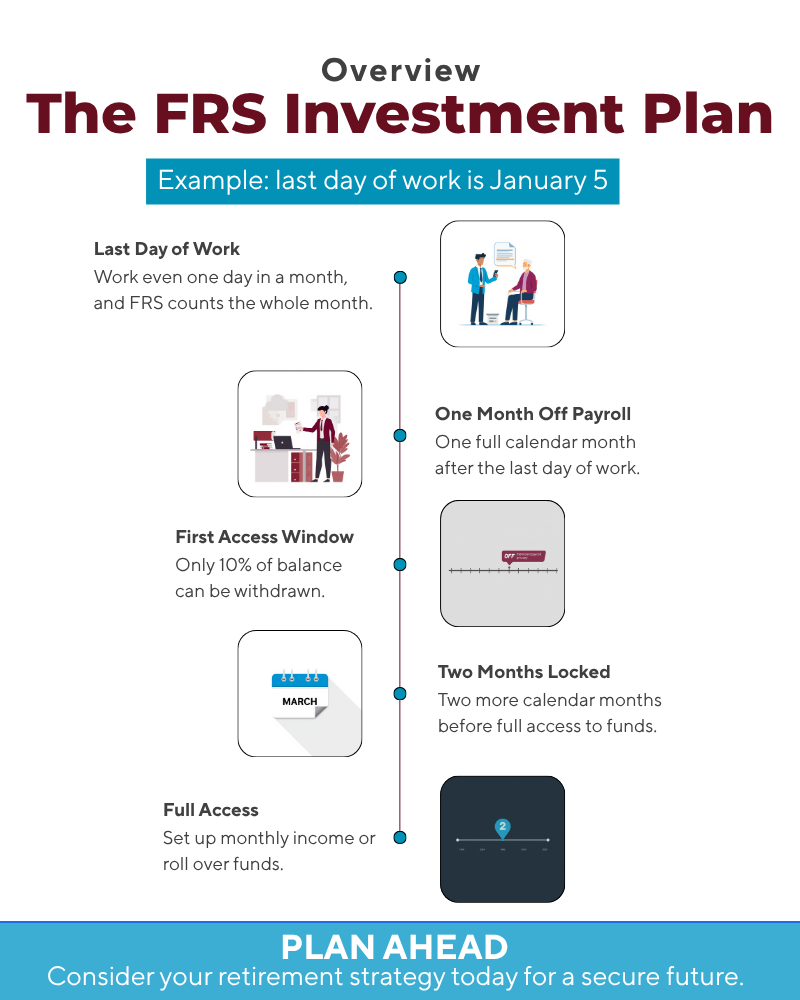

Two practical realities catch Investment Plan retirees off guard. First, timing: the rules require one full calendar month off payroll before any access to the account — and that first window allows only a 10% withdrawal, with full access two months after that. It routinely takes over three months to establish normal retirement income, which is why retiring at the end of a month (and having a deferred compensation account to bridge the gap) matters.

Second, the state's own Investment Plan newsletters regularly promote annuities as an income solution. Nelson's long-standing view: if you want a guaranteed lifetime check, stay in the Pension Plan — don't buy an insurance product to recreate one.

The Factors that Drive the Decision

When Nelson Financial Planning sits down with an FRS member to work through the election, these are the factors that actually drive the recommendation:

- Years of service and the benefit formula: the shorter you've served, the more the Pension's guaranteed income typically outweighs the Investment Plan's flexibility

- Age at election: members closer to retirement have a higher lump sum available under the Investment Plan than they would have earlier in their career.

- Timing of any switch: based on countless individual comparisons, a move to the Investment Plan tends to make sense either at the inception of a career or at the end — members mid-career (around 15 years of service) are usually best served waiting

- The second election: you get one switch per career, and using it — or losing it by entering DROP — is permanent. New hires must also make their first election within eight months or the state chooses for them by default

- Spouse's situation: survivor benefit options under the Pension Plan versus the Investment Plan's beneficiary flexibility

- Other retirement income sources: if you'll have substantial savings outside FRS, the Pension's predictability may be the right complement

- DROP eligibility and timing: DROP is only available to Pension Plan members, and for long-tenured members it changes the Pension Plan's value proposition significantly

- Appetite for market risk: this is behavioral as much as mathematical

None of these factors can be evaluated in isolation. They interact. The right answer for a 52-year-old teacher with 22 years of service and a younger spouse is genuinely different from the right answer for a 48-year-old law enforcement officer with 18 years of service and different income expectations. The second choice service at myfrs.com can model lump-sum scenarios — and a personalized analysis puts those numbers in the context of everything else.

The Drop Program: Better Than It Used to Be - If You Understand It

The Deferred Retirement Option Program (DROP) allows an eligible FRS Pension Plan member who has reached their normal retirement date to retire on paper — locking in their pension benefit — while continuing to work and draw a salary. The monthly pension checks accumulate in a separate account earning 4% annual interest, a rate the 2023 legislature raised from the 1.3% that applied from 2011 to 2023 (before 2011, it was 6.5%).

The 2023 session changed more than the rate. The maximum DROP period extended from 60 calendar months to 96 (8 years) for all membership classes, K-12 instructional personnel can add another 24 months for up to 120, and the old fixed entry window is gone — eligible members can now enter DROP at any time after reaching their normal retirement date.

DROP is not a bonus. As the Nelson FRS Booklet puts it: “DROP is simply holding your pension check while you continue to work for the State.” Your benefit is frozen at the entry-day calculation — years worked during DROP don't count toward the pension formula — which means every member should compare the DROP lump sum against what additional service years would add to the pension. Sometimes the extra years win.

The fine print matters just as much: entering DROP permanently closes your second election, commits you to a termination date, stops your 3% employee contribution (a small raise, in effect), and extensions up to the 96-month maximum require employer approval. And the payout decision at the end — direct withdrawal with mandatory 20% federal withholding versus a rollover to an IRA or the Investment Plan — carries penalty nuances that depend on your age and membership class. Direct DROP withdrawals recognize penalty exceptions at age 50 for special risk public safety officers and age 55 for regular class; an IRA rollover before 59½ erases those exceptions permanently.

For the complete guide — including when DROP makes sense and when it doesn't — see the full FRS DROP Program guide below.

Get the FRS Decision Guide - FREE

The State of Your Retirement - The Essential Guide for All State of Florida Employees

The complete guide to the Pension vs. Investment Plan election, DROP eligibility and timing, and what the legislative changes mean for your benefits. The FRS audience has the most to lose from a wrong decision — this guide exists so members don't make one uninformed.

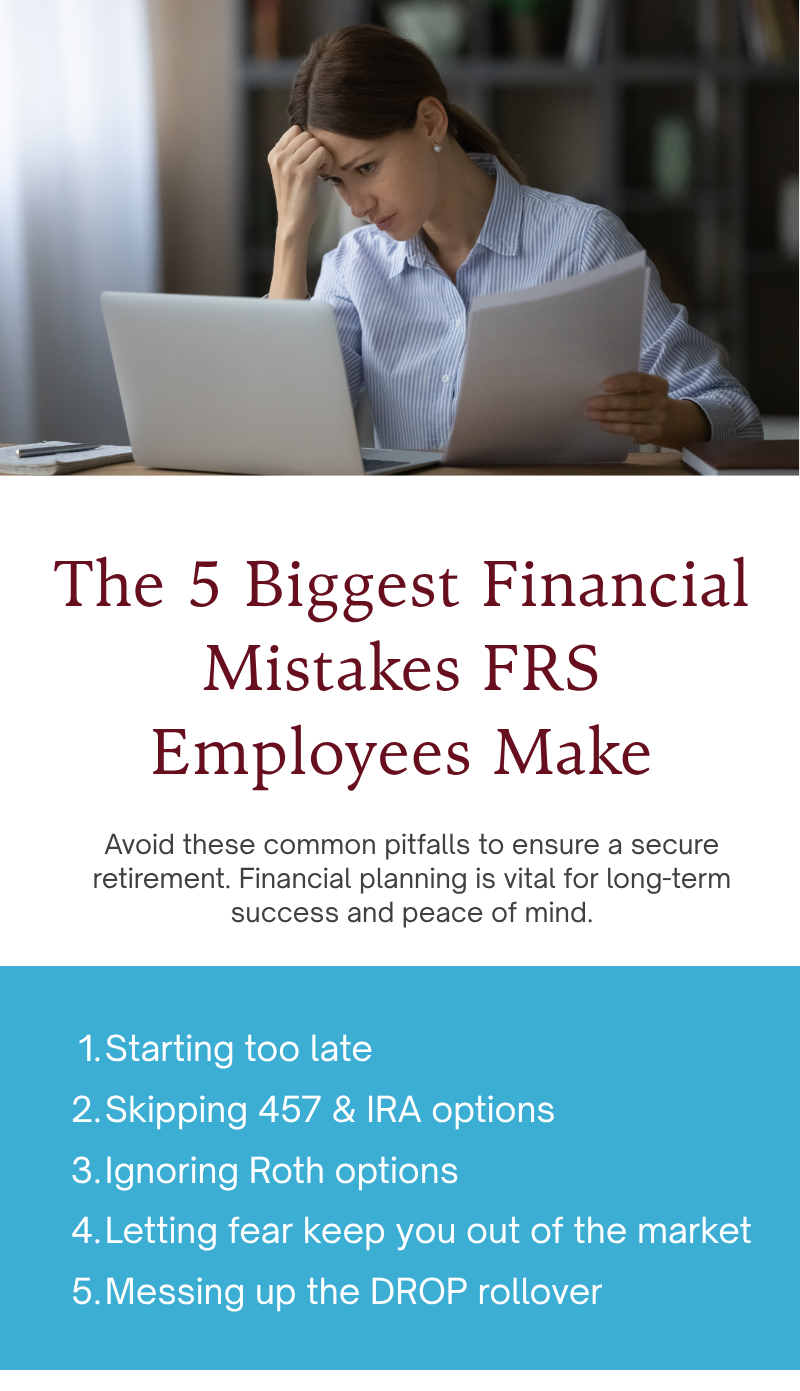

The 5 Biggest Financial Mistakes FRS Employees Make

Zach Keister, Certified Financial Fiduciary™ — a former firefighter at Station 32 in Indianapolis before joining Nelson — spends his weeks meeting with teachers, firefighters, and government employees across Florida: school-break reviews, fire station visits, one focused conversation at a time. When he tells a first responder that their service protects the community and his job is to protect their financial future, he means it from experience. These are the five mistakes he sees most:

STARTING TOO LATE

Your pension is great — but for most retirees, it is not enough alone. A small monthly investment early makes a massive difference later.not using 457, 403(b), or ira options

Deferred compensation deserves special attention: 457 plans have no 10% early-withdrawal penalty at any age after separation — a benefit almost nothing else offers, and one that's forfeited if the account is rolled to an IRA before 59½. These accounts also bridge the Investment Plan's three-month access gap at retirement.skipping roth options

Roth accounts let you pay taxes now — often while you're in a lower bracket — so the money comes out tax-free later, a powerful complement to a fully taxable pension check.LETTING FEAR KEEP YOU OUT OF THE MARKET

Headlines are real, and so is financial overwhelm — but doing nothing is the most expensive option.messing up the drop rollover

The most preventable — and most costly — mistake: mandatory withholding, penalty traps, and forfeited exceptions that careful sequencing avoids entirely.As Zach puts it: as a Certified Financial Fiduciary™, his role is to sit on your side of the table — offering guidance that's in your best interest, not anybody else's. The conversation is free, with no obligation.

The Forgotten Benefit: The Health Insurance Subsidy

Eligible FRS retirees — Pension Plan and Investment Plan alike — qualify for a monthly Health Insurance Subsidy of $7.50 per year of service, between $45 and $225 per month, plus a county portion where offered (Orange County pays one). Nelson Financial Planning has found this unclaimed money for numerous retirees, because the state only pays six months in arrears: every month beyond that without filing the certification forms is money forfeited forever.

In-Depth Guides: Florida Retirement System

Our in-depth FRS guides:

- FRS DROP Program: How the Deferred Retirement Option Works in 2026

- FRS Investment Plan Explained: Flexibility, Risk, and Leaving It to the Kids (coming soon)

- FRS Benefit Calculation: How to Estimate Your Pension

- FRS Pension Plan Explained: The Guaranteed Check-a-Month (coming soon)

- FRS Pension vs Investment Plan: Which is Right for You? (coming soon)

Frequently Asked Questions

What is the Florida Retirement System?

The Florida Retirement System is a public pension system covering Florida state employees, teachers, law enforcement officers, firefighters, and other government workers. Eligible employees choose between the FRS Pension Plan — a defined benefit plan that provides a guaranteed monthly income for life — and the FRS Investment Plan — a defined contribution plan where the employer contributes a set percentage and the member directs investments. For most members, the election is irreversible.

Should I choose the FRS Pension Plan or the Investment Plan?

The right choice depends on your years of service, salary history, proximity to retirement, spouse's situation, Social Security earnings history, other retirement assets, and appetite for market risk. The Pension Plan offers income security that cannot be outlived; the Investment Plan offers portability and flexibility. Nelson Financial Planning provides individualized FRS decision analyses — including Social Security coordination — for Florida government employees. Schedule a free review - give us a call today to book.

Is DROP extra money on top of my pension?

No — this is the most common FRS misconception. DROP is your own pension benefit, frozen at the entry-day calculation and held in an account earning 4% interest instead of being paid monthly. Years worked during DROP don't increase the pension formula, which is why every member should compare the DROP lump sum against what additional service years would add.

How long can I participate in DROP, and what does it pay?

Up to 96 calendar months (8 years) for all membership classes, and up to 120 months for K-12 instructional personnel. DROP balances earn 4% annually — raised from 1.3% effective July 1, 2023. Since 2023, eligible members can enter DROP at any time after reaching their normal retirement date.

Can I roll over my FRS Investment Plan if I leave state employment?

Yes. The FRS Investment Plan is portable and can be rolled to an IRA or another qualified plan when you leave state employment. The FRS Pension Plan has a refund of contributions option for members who leave before reaching retirement eligibility, but the guaranteed monthly benefit is only available at retirement. Nelson Financial Planning evaluates rollover options and tax implications as part of any FRS transition analysis.

Does Nelson Financial Planning charge FRS members for a consultation?

No. FRS conversations have been a free service to state employees since 1984 — no consulting fees, no account minimums, no obligation. Every advisor is a Certified Financial Fiduciary™, legally and ethically bound to act in your best interest.

Navigating an FRS decision? Get expert guidance - no account minimums

Nelson Financial Planning has guided Florida government employees through FRS elections for decades. Schedule a free FRS planning review.