FRS Drop Program

How the Deferred Retirement Option Program Works in 2026

DROP is one of the most misunderstood benefits in the entire Florida Retirement System — and the misunderstanding usually starts with what people think it is.

DROP is not extra money. It's not a bonus for long service. It's a holding bin for a pension check that already belongs to the member. Once that clicks, every other DROP decision — when to enter, how long to stay, what to do with the money at the end — gets a whole lot clearer.

And here's why this page exists: the rules changed significantly in 2023, and much of what Florida's teachers, law enforcement officers, firefighters, and government employees remember hearing about DROP is now out of date. The interest rate tripled. The maximum participation window went from five years to eight. The old entry deadline disappeared. For members approaching their normal retirement date, DROP is a genuinely better deal than it was — but only for those who understand what it actually does.

This guide is part of Nelson's complete Florida Retirement System planning guide — the full picture on the Pension Plan, the Investment Plan, and how DROP fits between them.

What is the FRS DROP Program?

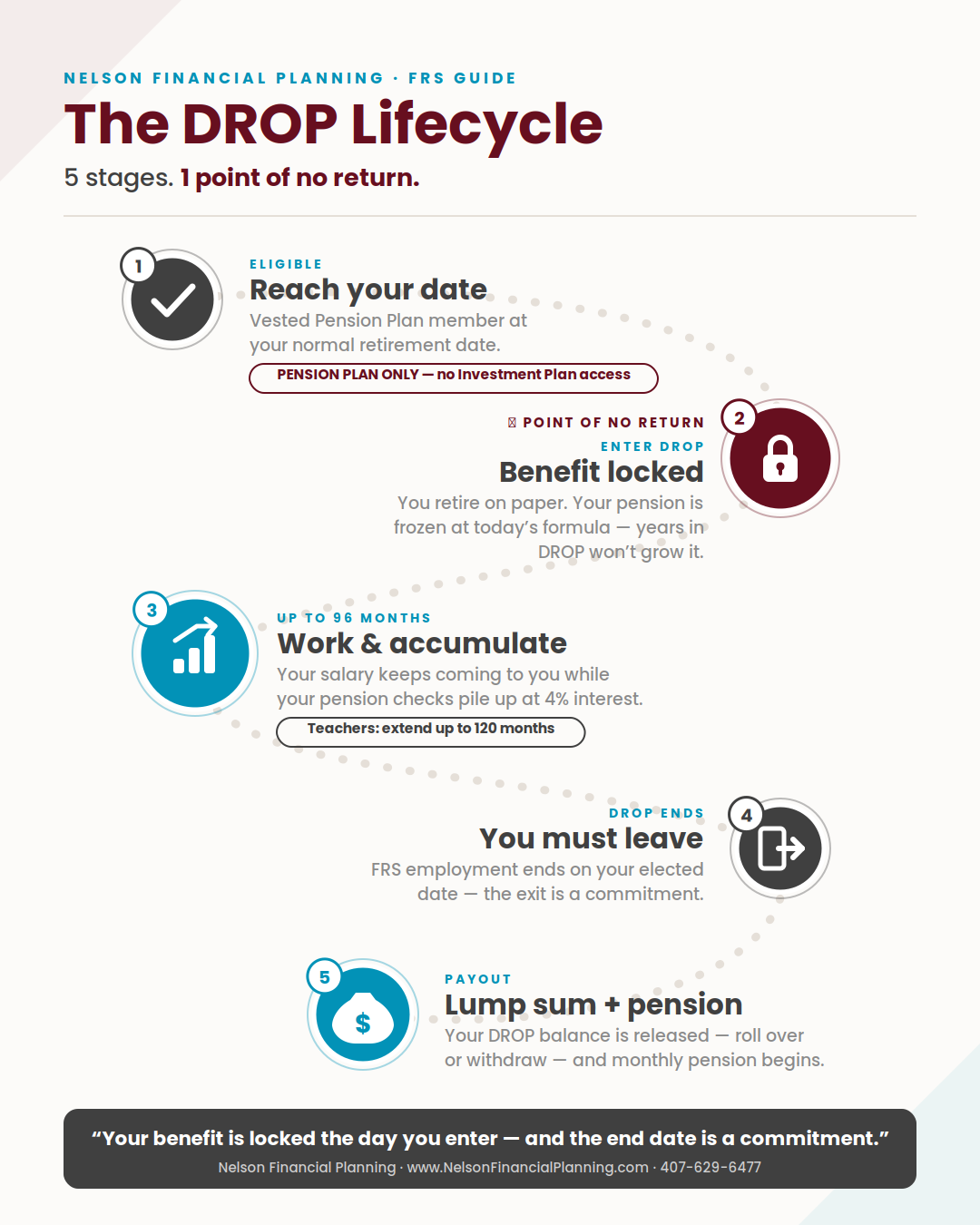

The Deferred Retirement Option Program (DROP) allows a vested FRS Pension Plan member who has reached their normal retirement date to formally retire — locking in their pension benefit — while continuing to work for their FRS employer for up to 96 months. During that period, the monthly pension checks the member would have received accumulate in a separate account earning 4% annual interest. When the DROP period ends, the member must leave FRS employment, the accumulated lump sum becomes available, and monthly pension payments begin.

That's the whole mechanism. The member retires on paper, keeps working and collecting a paycheck, and their pension piles up in the background instead of being paid out.

One critical eligibility note before going further: DROP is only available to FRS Pension Plan members. Employees who elected the FRS Investment Plan are not eligible — which is one of the reasons the Pension vs. Investment Plan election needs to be made with the full picture in mind, including whether DROP access matters down the road.

The Holding Bin for a Pension Check

Nelson Financial Planning has been explaining DROP to Central Florida government employees the same way for years: think of it as a holding bin.

When a member enters DROP, they retire under the FRS Pension Plan based on their years of service at that moment. The benefit is calculated using the standard pension formula — years of service × percentage value × average final compensation — and locked in at that amount. Instead of being mailed out every month, that check accrues in the DROP account.

Two things follow from that, and they're the two things members most often miss:

The pension is frozen at the entry amount. Years worked during DROP do not count toward the pension calculation. A member who enters DROP with 30 years of service and works 8 more years still receives a pension based on 30 years — not 38. For some members, the additional service years would grow the pension more than the DROP lump sum is worth. That comparison — extra service years versus the accumulated lump sum — is the single most important calculation to run before signing the paperwork, and it comes out differently for different people.

The clock has a hard stop. At the end of the elected DROP period, the member must terminate FRS employment. Entering DROP is a commitment to retire on a specific date. Members need to be genuinely ready for that. (One narrow exception from 2026 legislation: certain elected officers — not legislators — who complete DROP may receive their accumulation at age 59½ without leaving office. It does not apply to regular members.)

What Changed in 2023 - and Why It Matters Now

The 2023 Florida legislative session made DROP meaningfully more attractive in an effort to retain experienced FRS employees. Anyone whose understanding of DROP predates these changes is working from the wrong playbook:

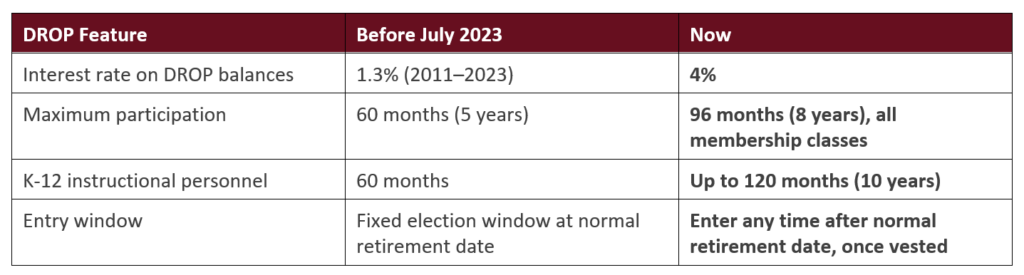

A little historical context, because it explains how DROP's reputation got stuck: before 2011, DROP monies earned a guaranteed 6.5%. The 2011 legislature slashed that to 1.3%, and for the next twelve years, the honest analysis was that the interest rate really undermined DROP's value. The 2023 increase to 4% doesn't restore the glory days — but it changes the math substantially, especially over an 8-year window with compounding.

The entry window change matters just as much. Under the old rules, members who missed their election window lost DROP months permanently. Now, an eligible member can enter DROP at any time after reaching their normal retirement date and meeting vesting requirements. That flexibility turns DROP from a use-it-or-lose-it deadline into a genuine planning decision.

The Fine Print Most FRS Members Miss

Beyond the headlines, a handful of details consistently surprise members — usually after it's too late to do anything about them:

Entering DROP closes the door on the Investment Plan. FRS members get one second election to switch between the Pension Plan and the Investment Plan during their career. Entering DROP permanently ends that option.

The 3% employee contribution stops. DROP participants no longer pay the 3% required employee contribution — a small raise, in effect, during the DROP years.

Extensions need employer approval. A member who initially elects fewer than 96 months can extend up to the maximum, but only with their employer's sign-off. Ending DROP earlier than planned doesn't require approval.

COLA treatment follows the pension rules. The pension benefit accumulating in DROP reflects the cost-of-living adjustment rules tied to the member's service before and after July 2011 — another reason two members with identical salaries can see very different DROP outcomes.

DROP years don't count toward the state's Health Insurance Subsidy. The state's HIS portion — $7.50 per year of service, up to $225 per month — is calculated excluding DROP time, though county portions, where offered (Orange County pays one), do include DROP years. The subsidy is also only paid six months in arrears, so retirees who never file the certification forms forfeit everything earlier. One more line item members tend to discover late.

A 2026 improvement worth knowing: effective July 1, 2026, House Bill 5205E established a minimum 1.5% annual cost-of-living adjustment for eligible Special Risk Class retirees — the first COLA improvement since the 2011 suspension. Retirees qualify once they have been retired at least five years, with six years of Special Risk Class creditable service (eight years for those initially enrolled on or after July 1, 2011). Members enrolled before July 2011 receive the greater of 1.5% or their blended formula rate; those enrolled later receive the flat 1.5%.

(Source: Florida Division of Retirement, Information Release 26-241, June 29, 2026.)

When DROP Makes Sense — and When It Doesn't

DROP works best for members who plan to keep working several years past their normal retirement date anyway, and whose locked-in benefit is strong enough that freezing it now beats continuing to accrue. For that member, DROP means collecting a salary and banking a pension simultaneously — with the state guaranteeing 4% on the balance.

DROP makes less sense when a member is close to a meaningfully higher benefit tier that additional service years would earn, when workforce flexibility matters more than the lump sum, or when the member isn't actually prepared to commit to a termination date.

As Joel Garris puts it on the Dollars & Sense podcast: the right answer for a 52-year-old teacher with 22 years of service and a younger spouse is genuinely different from the right answer for a 48-year-old law enforcement officer with 18 years and no spouse. These aren't generic decisions. They depend on the benefit formula, the years of service, the household's other assets, Social Security timing, and the survivor option selected at retirement — all of which interact.

What Happens to the DROP Money at the End

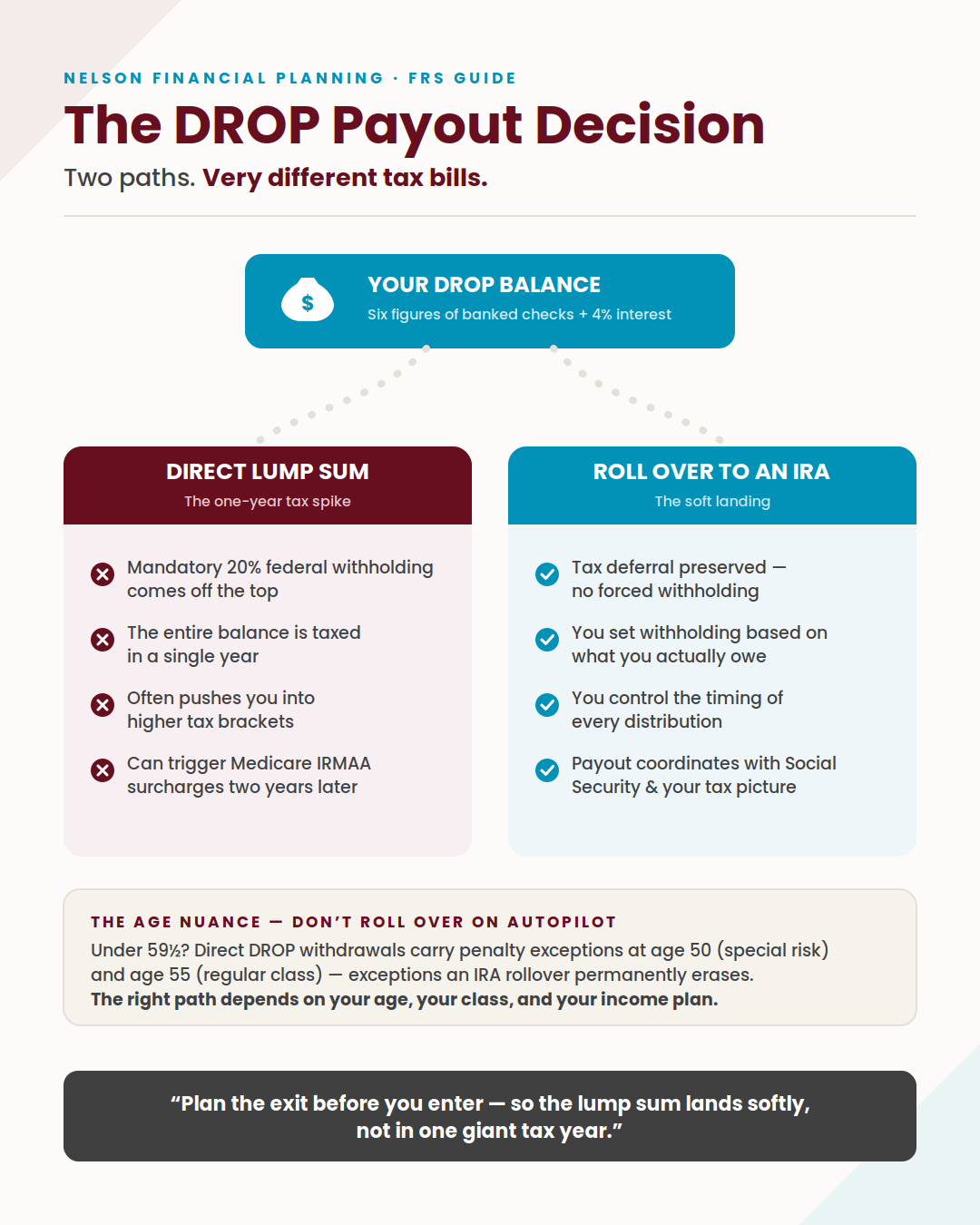

When the DROP period ends and employment terminates, the accumulated balance — often six figures after several years of banked pension checks plus interest — becomes available. This is where good planning pays for itself, because the tax treatment of the next step varies enormously.

Taking the balance as a direct lump sum triggers a mandatory 20% federal withholding and stacks the entire amount into a single tax year — frequently pushing a retiree into higher brackets and, for higher-income households, potentially into Medicare IRMAA surcharge territory two years later. Rolling the balance into an IRA instead preserves tax deferral, allows the retiree to set their own withholding as they draw income, and keeps distribution timing under their control. Because DROP monies are retirement funds, early-withdrawal penalty rules can also apply depending on age and circumstances — one more reason the rollover decision should be made deliberately, not by default.

The typical path Nelson Financial Planning walks clients through: coordinate the DROP payout with the first years of retirement income, the Social Security claiming decision, and the household's tax picture — so the lump sum lands softly instead of creating a one-year tax spike.

How Nelson Financial Planning Helps FRS Members

Nelson Financial Planning has spent 40+ years serving Central Florida, and Florida Retirement System members — teachers, law enforcement, firefighters, and state and county employees — have always been a core part of that work. The firm literally wrote the book on it: the FRS Booklet, now in its 5th edition, covers the Pension Plan, the Investment Plan, DROP, and the legislative changes that have reshaped all three.

Every advisor guiding these decisions is a Certified Financial Fiduciary™ — which means something specific: they have completed dedicated fiduciary training and are legally and ethically bound to act in clients' best interests at all times. For an FRS member weighing an irrevocable decision like DROP entry, that distinction matters. There are no account minimums to meet. The advice is the product.

Request a Copy of Our Free FRS Booklet

The State of Your Retirement - The Essential Guide for All State of Florida Employees

Frequently Asked Questions About the FRS Drop Program

What is the FRS DROP Program?

The Deferred Retirement Option Program (DROP) allows vested FRS Pension Plan members who have reached their normal retirement date to retire on paper — locking in their pension benefit — while continuing to work for an FRS employer for up to 96 months. The monthly pension payments accumulate in a separate account earning 4% annual interest, and the lump sum becomes available when the member terminates employment at the end of the DROP period.

How long can you participate in DROP?

Up to 96 calendar months (8 years) for all FRS membership classes — extended from 60 months by the 2023 Florida legislature. K-12 instructional personnel, such as public school teachers, can extend an additional 24 months for a maximum of 120 months (10 years). Members who initially elect a shorter period may extend up to the maximum with employer approval.

What interest rate does DROP pay in 2026?

DROP balances earn 4% annually, effective July 1, 2023. From 2011 to 2023 the rate was 1.3%, and before 2011 it was 6.5%. The 2023 increase meaningfully improved DROP's value, particularly over the longer 96-month participation window.

Is DROP extra money on top of your pension?

No — and this is the most common misconception. DROP is not a bonus; it is the member's own pension benefit, calculated and frozen at DROP entry, held in an interest-bearing account instead of being paid monthly. Years worked during DROP do not increase the pension calculation. For some members, additional service years would grow the pension more than the DROP lump sum is worth — a comparison every member should run before enrolling.

Who is eligible for DROP?

FRS Pension Plan members who are vested and have reached their normal retirement date. Since 2023, eligible members can enter DROP at any time after that point — the old fixed election window no longer applies. FRS Investment Plan members are not eligible for DROP, which is one reason the Pension vs. Investment Plan election deserves careful analysis.

Does entering DROP affect the option to switch to the Investment Plan?

Yes. FRS members receive a second election to move between the Pension Plan and Investment Plan during their career, and entering DROP permanently closes that option. DROP entry also commits the member to terminating FRS employment at the end of the DROP period.

What happens to DROP money when the DROP period ends?

The member must leave FRS employment, and the accumulated balance becomes available either as a direct payout — subject to mandatory 20% federal withholding and full taxation in a single year — or as a rollover to an IRA or the FRS Investment Plan, which preserves tax deferral and lets the retiree control withholding and distribution timing. Members under 59½ should note that direct DROP withdrawals qualify for penalty exceptions at age 50 (special-risk public safety officers) or age 55 (regular class) — exceptions that are lost once the money moves to an IRA. Most members benefit from coordinating this decision with their broader tax and income plan; Nelson Financial Planning includes DROP payout planning in every free FRS planning review.

Is DROP worth it?

It depends on the member's specific numbers. DROP tends to favor members who plan to work several more years anyway and whose locked-in benefit is strong. It tends to work against members close to a higher benefit tier that more service years would earn. The decision requires comparing the frozen-pension-plus-lump-sum path against the keep-accruing path using the member's actual benefit formula, service years, and household situation — there is no universal answer.

Schedule Your Free Conversation Today

No account minimums. No obligation.

Planning your retirement savings as a member of FRS is a very intricate process. Depending on your age, years of service, FRS choices, and your deferred compensation account, the composition of your retirement benefits will be different. We encourage you to contact us to schedule your complimentary, no-obligation conversation about planning your retirement income.