updated December 2025

Why Tax Planning Matters More Than Ever – and the Hidden Cost of “Tax-Free” Retirement

At the start of the year, taxes are on everyone’s minds. The shared goal is to reduce your tax liability and keep more money in your wallet. There are many avenues for doing so, and a financial advisory firm like Nelson Financial Planning is well-equipped to help you find and take full advantage of the most relevant ones.

For years, financial success has been measured by how much you earn, how diligently you save, and how aggressively you invest. Those factors matter, but they miss a critical piece of the puzzle – how much of your money you actually keep. Taxes quietly influence nearly every financial decision, especially as retirement approaches, and ignoring that reality can create consequences that ripple for decades.

Recent surveys reveal that 90 percent of households with assets exceeding $250,000 want tax planning advice included in the financial services they receive. This notable shift in client priorities places tax advice and strategy higher on the list than retirement planning! As consumers become increasingly savvy about their finances, they want to optimize their tax situation alongside their investment strategies.

“You only get to spend what you keep after taxes. It’s always about the net, not the gross.” – Joel

That statement captures why tax planning matters, particularly for individuals over 50 who are transitioning from accumulation into distribution. Retirement planning without tax planning is incomplete, no matter how strong the portfolio looks on paper.

Unlike investment returns, taxes are one variable you can partially control with foresight. Thoughtful tax planning doesn’t eliminate taxes, yet it can dramatically reshape retirement outcomes. The goal isn’t perfection. Instead, the objective is clarity, predictability, and strategic coordination between income, investments, and the tax code.

While specific guidance is always best, general advice is a good place to start. Today, we’re covering traditional IRAs vs. Roth IRAs and the Employer Retention Credit (ERC).

What is Tax Planning – and Why It’s Different from Tax Preparation

A common misconception equates tax planning with filing a return accurately. While compliance matters, tax planning operates in a different time frame entirely. Filing looks backward. Planning looks forward. One documents what already happened; the other evaluates what should happen next.

Tax planning involves evaluating income sources, investment vehicles, withdrawal sequencing, timing strategies, and legislative thresholds before decisions become permanent. It also requires understanding how one change affects everything else. Adding income does not merely increase tax owed; it can alter Medicare premiums, Social Security taxation, capital-gain treatment, and deduction eligibility.

Christina Lamb highlighted this nuance during the podcast discussion:

“It’s not just about adding income to your return. You have to look at whether it affects Social Security, Medicare premiums, net investment income tax, or itemized deductions that are income-based.”

That interconnectedness explains why tax planning has surged in importance. According to consumer research referenced in the episode, tax strategy has surpassed retirement planning as the most requested financial service among affluent households. Investors increasingly understand that managing taxes is not optional – it is foundational.

Why Tax Planning Has Become a Priority for Retirement-Focused Investors

The financial landscape has changed. Information is more accessible, investment options are more transparent, and consumers arrive better informed than ever before. As a result, expectations have shifted. People no longer want generic advice. They want coordinated guidance that reflects the full financial picture.

Garris noted this evolution clearly:

“Clients are far more educated about investments today. What they’re demanding now is tax strategy, because that’s where the impact is.”

Despite that demand, many large financial institutions explicitly disclaim responsibility for tax advice. Statements often include language instructing clients to “consult your tax preparer,” even though those same firms control investment decisions that directly influence tax outcomes. That disconnect leaves retirees exposed to unnecessary inefficiencies.

Effective tax planning services bridge that gap by integrating investment strategy with real tax modeling. This approach recognizes that retirement income planning is not static. It evolves annually, sometimes quarterly, and must respond to both personal circumstances and legislative change.

The Appeal – and Reality – of “Tax-Free” Retirement

The phrase “tax-free retirement” is compelling. Who wouldn’t want income untouched by the IRS? Marketing campaigns know this, which is why the concept is frequently simplified, amplified, and stripped of context. The most common path toward tax-free income involves Roth accounts, particularly Roth IRA conversions.

Roth conversions can be powerful tools, yet they are often misunderstood. Converting tax-deferred assets into after-tax accounts requires recognizing income immediately. That income is taxed at current marginal rates, regardless of future expectations.

On the podcast, Garris framed the issue with a simple but effective analogy:

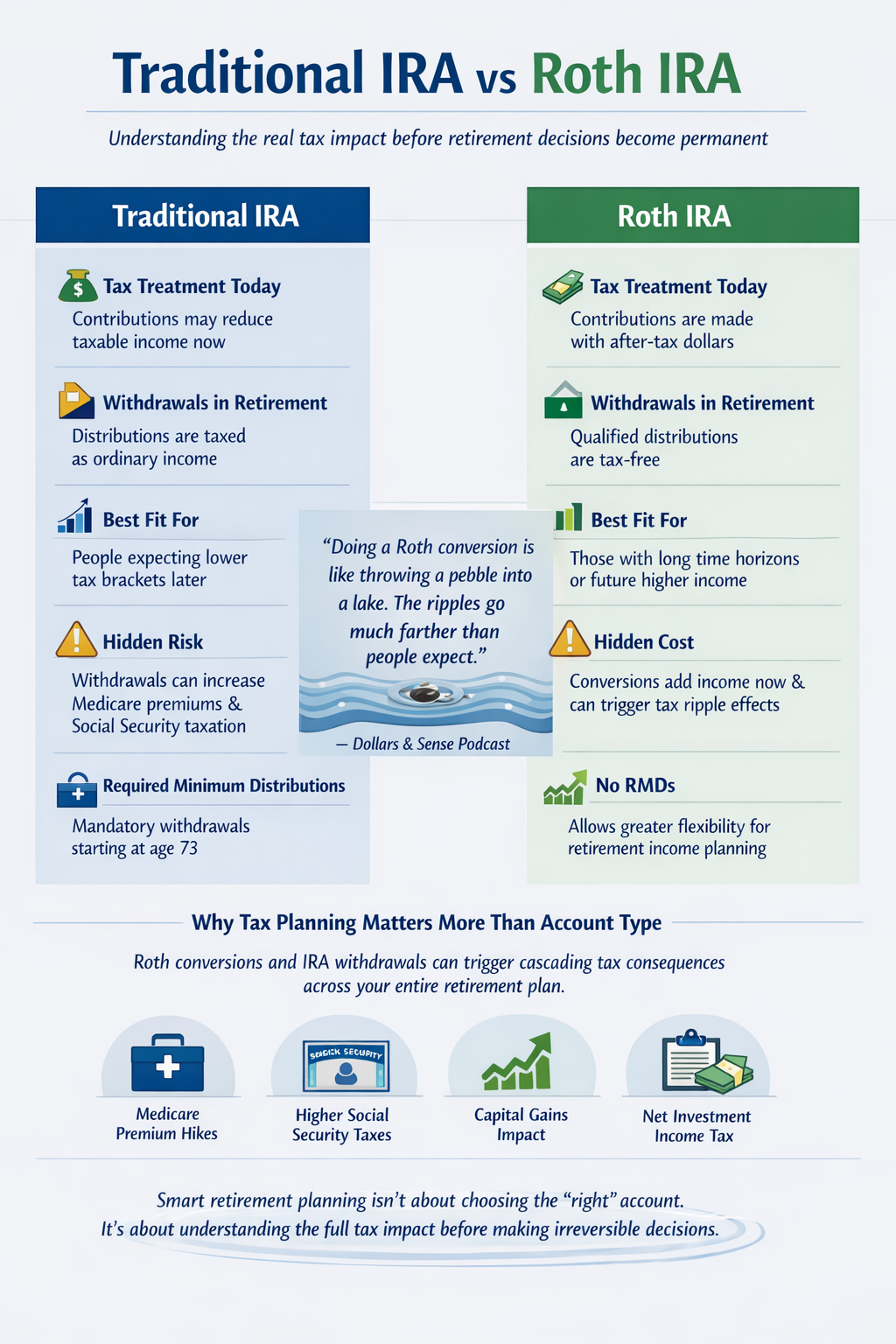

“Doing a Roth conversion is like throwing a pebble into a lake. You see the ripples, and they travel much farther than people expect.”

Those ripples extend well beyond the conversion year. A single decision can increase Medicare IRMAA surcharges, cause more Social Security benefits to become taxable, elevate capital-gains exposure, or trigger the Net Investment Income Tax. The cost of the conversion is not limited to the check written to the IRS.

Choosing Between a Traditional and Roth IRA: Understanding the Tradeoffs

Retirement plans go well beyond employer-sponsored 401(k)s. Traditional and Roth IRAs are two pillars of retirement planning that offer distinct tax advantages and considerations. Understanding the differences between each one can help you make the best decisions for your financial future after retirement.

At a basic level, the distinction is straightforward. Traditional IRA contributions may reduce taxable income today, but withdrawals are taxed later. Roth IRAs reverse that equation: taxes are paid upfront, and qualified withdrawals are tax-free. Contribution limits are similar, with additional catch-up allowances for individuals over 50.

However, the simplicity ends there. Roth IRAs impose income eligibility thresholds, and Roth conversions introduce complex timing considerations. For retirees already living within lower tax brackets, converting assets that would later be taxed at 12% into income taxed at 22% can erode long-term efficiency.

Lamb addressed this directly during the episode:

“If you’re already retired and sitting comfortably in a lower bracket, coverting income at a higher marginal rate doesn’t automatically make sense.”

Tax planning strategies must evaluate not only current rates, but also projected income needs, longevity, survivor considerations, and opportunity cost. Paying taxes early reduces capital available for growth. That lost compounding matters, especially when markets perform well.

Defer Taxes With a Traditional IRA

A traditional IRA is an individual retirement account with deductible contributions. The amount you invest into your account is subtracted from your taxable income, providing an upfront tax break. However, this immediate benefit comes with a long-term consideration: distributions taken in retirement are taxed as ordinary income. This setup may appeal to you if you anticipate being in a lower tax bracket during retirement when your distributions will be taxed at a lower percentage.

Enjoy Tax-Free Growth With a Roth IRA

A Roth IRA is funded with after-tax dollars, meaning contributions are not tax-deductible. The trade-off here is the potential for tax-free growth and tax-free withdrawals in retirement, assuming certain conditions are met. This makes the Roth IRA an attractive option if you expect your tax rate to be higher in retirement or you value the flexibility of tax-free withdrawals.

Eligibility and Contribution Limits

Both traditional and Roth IRAs have a contribution limit of $7,000 per year (or $8,000 for those 50 years old and above, thanks to the catch-up contribution). However, the Roth IRA includes income limits that restrict high earners from contributing directly to a Roth. The traditional IRA does not impose income limits for contributions, though income levels and participation in employer-sponsored plans may affect tax deductibility.

The Cost of a Tax-Free Retirement

The chance to enjoy a tax-free retirement often draws attention to the Roth IRA, especially with the option of converting a traditional IRA to a Roth. Such conversions allow taxpayers to pay taxes on pre-tax assets now in exchange for tax-free withdrawals later. The Roth’s tax-free growth potential is particularly compelling for younger investors, given the longer time horizon for investments to grow.

However, Roth conversions add to your taxable income for the year, potentially bumping you into a higher tax bracket and affecting the taxation of Social Security benefits or Medicare premiums. Clearly, deciding between these types of IRAs – or determining the suitability of a Roth conversion – requires careful analysis of your current tax situation, expected future tax rates, and retirement goals. Your decision is further complicated by ever-changing tax laws. For these reasons, it’s best to consult a tax professional before making your decision.

Timing Matters More Than Predicting Future Tax Rates

A frequent justification for aggressive Roth conversions centers on fears of future tax increases. While rates may rise, timing remains the dominant variable. For many retirees, the early years of retirement present unique planning opportunities due to lower earned income and higher standard deductions.

Converting too much, too quickly can push income into higher brackets unnecessarily. Converting strategically over multiple years may achieve similar long-term benefits with less disruption.

This is where sophisticated modeling becomes essential. As Lamb emphasized,

“You have to run the actual tax return. Estimates don’t capture the ripple effects.”

Effective tax planning services rely on real software projections, not theoretical spreadsheets. Each scenario must be tested against current law and personal circumstances.

The Employee Retention Credit (ERC)

The Employee Retention Credit (ERC) has played a significant role in pandemic relief efforts, aiding employers who kept their workforce employed during the challenging times of 2020 and 2021. This tax credit, offering up to $26,000 per employee, aimed to offset the financial burden for businesses striving to maintain their operations and workforce amid economic uncertainty.

Initially, the ERC served as a critical support mechanism, incentivizing businesses to retain employees while the economy was partially shuttered. Eligibility for this credit was specific, targeting businesses that saw a considerable decrease in gross receipts or were unable to operate as usual due to mandated shutdowns. These qualifications aimed to direct assistance toward the businesses most affected by the pandemic’s economic fallout. In addition, the distinction between qualified wages and the interplay with other relief options like the Payroll Protection Program (PPP) highlighted the need for careful consideration before claiming the ERC.

However, the ERC’s popularity gave rise to opportunistic tax preparation firms charging significant fees to help businesses claim this credit. This development raised concerns, as some firms pursued aggressive tactics, sometimes leading businesses to claim the credit improperly.

The IRS’s response to this has included halting the processing of claims and proposing a settlement offer. This would allow businesses to retract their claims without penalty, acknowledging the challenges and confusion surrounding eligibility and proper claim processes.

Taxes and Retirement Income: The Hidden Interactions

Retirement income rarely comes from a single source. Social Security, pensions, investment withdrawals, required minimum distributions, and part-time earnings often overlap. Each stream interacts differently with the tax code.

Social Security taxation thresholds have not been inflation-adjusted since the 1980s, meaning more retirees face taxation today than originally intended. Medicare premiums increase based on income levels, and small changes can have outsized effects.

These interactions explain why tax planning cannot be an afterthought. Decisions made in isolation – without considering Medicare or Social Security – often produce unintended consequences that persist for years.

Why Comprehensive Tax Planning Services Matter

True tax planning integrates investments, retirement income, and tax preparation under one coordinated framework. That integration allows advisors to anticipate issues before they appear and adjust strategies proactively.

Nelson Financial Planning’s approach emphasizes forward-looking analysis rather than reactive fixes. By aligning tax planning services with retirement objectives, clients gain clarity rather than complexity.

As the podcast discussion revealed, the most successful retirees are not those who eliminate taxes entirely, but those who understand them thoroughly.

The Goal of Tax Planning is Control, Not Elimination

Taxes are unavoidable. Surprises are not. The purpose of tax planning is not to avoid responsibility but to manage it intelligently. Control replaces guesswork. Strategy replaces speculation. Confidence replaces anxiety.

A well-structured plan evaluates tradeoffs honestly. It acknowledges costs upfront. It adapts as laws change. Most importantly, it reflects personal goals rather than marketing promises.

Tax planning, when done correctly, becomes a stabilizing force in retirement. It transforms uncertainty into informed decision-making and supports the long-term sustainability of income.

Final Thoughts: Why Tax Planning Matters Now

Retirement planning has entered a new era. Longevity has increased. Tax laws have grown more complex. Marketing noise has intensified. In that environment, tax planning provides clarity.

The question is no longer whether tax planning matters. The question is whether your strategy accounts for the full picture. Those who address taxes proactively retain flexibility. Those who ignore them surrender it.

As Dollars & Sense consistently emphasizes, smart financial decisions are rarely about doing more. They are about doing what aligns.

Nelson Financial Planning’s Unique Approach

At Nelson Financial Planning, we integrate tax planning with our other financial advisory services for retired clients. With 40 years of industry experience, we are uniquely positioned to offer sound tax advice. Our comprehensive approach goes beyond simple tax return preparation to include trustworthy advice and accurate projections, helping you make informed decisions about your investments, retirement, and tax strategies.

When you’re ready to change your life with a successful financial plan that provides peace of mind for the future, please contact our office in Winter Park, FL.

Your retirement deserves more than guesswork. It deserves a strategy.

Schedule your complimentary consultation with one of our financial planners today!

Get a free copy of our book and workbook Next Gen Dollars & Sense

Unlock the secrets to financial success with Joel J. Garris’ insightful book, designed to equip you with the essential tools and strategies needed to take control of your financial future. Whether you’re just beginning your financial journey or approaching retirement, this book offers a comprehensive guide to help you build a solid financial plan that aligns with your goals.

ABOUT JOEL GARRIS, JD, CFP®

Joel J. Garris, JD, CFP®, is the President and CEO of Nelson Financial Planning in Orlando, FL and the voice behind the Dollars & Sense podcast. A seasoned financial advisor with over 20 years of experience, Joel helps everyday investors make sense of complex markets with clarity and confidence.

When he’s not simplifying retirement strategies or decoding economic trends, he’s probably on air delivering straight-talk financial advice – no fluff, just facts.

Credible Reference Sources Used

• IRS Retirement Plans FAQs

• Social Security Benefits Retirement Planner – Taxes

• Medicare Costs

• Kiplinger: IRA Conversion to Roth IRA Rules

- 8 Wonders1

- Bank Investments3

- Beating Inflation1

- Budget for Retirement5

- Corporate Transparency Act2

- Digital Currency1

- Energy Tax Credits1

- ESG Funds1

- Featured Blog0

- Financial Planning14

- Financial Success5

- Importance of Dividends2

- Investment Diversification1

- Investment Portfolio6

- Investment Strategy4

- IRA1

- Joel Garris1

- Nelson Financial Planning7

- Net Worth Improvement1

- Next Gen Dollars and Sense1

- One Big Beautiful Bill Act (OBBBA)1

- Pension Plans1

- Podcast Transcripts17

- Retirement “Secure” Act2

- Retirement Income Planning3

- Retirement Planning7

- Retirement Regrets5

- Social Security4

- Tax Liability3

- Tax Planning7

- Year-End Tax Changes3